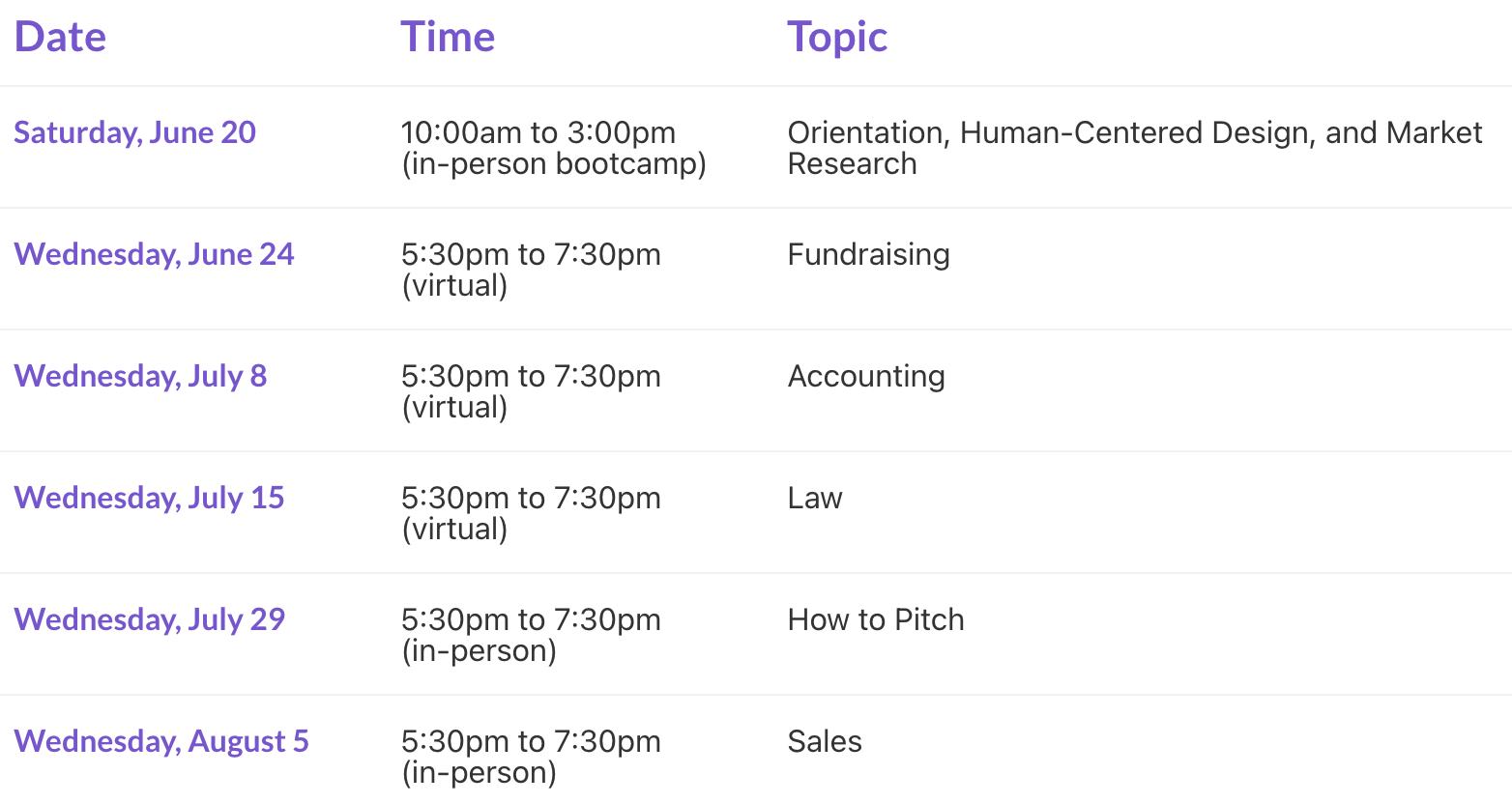

Tax season for entrepreneurs with their own business can look different case by case. Whether you are a sole proprietor, or have incorporated your business, you will have to file the income/losses associated with your business for tax purposes. These articles will explain how you are taxed on your income from your business, which expenses are and are not deductible for tax purposes, and go a bit in depth on more specific topics.

Business Income/Losses vs Capital Gains/Losses

It is important to determine whether your transactions during the year are considered business income/losses or a capital gains/losses, as they are treated differently when you file your taxes.

| Business Income/Losses | Capital Gains/Losses |

| When you bought the property, you had the intention of reselling it | When you bought the property, you had the intention of deriving benefits from using it long-term |

| The transaction was similar to what’s conducted in your normal course of business | The transaction was not something that normally occurs in your course of business |

| Sold inventory | Sold a fixed asset |

When taxing the gains/losses incurred from business or capital transactions, note that there are a couple of differences between the two.

| Business Income/Losses | Capital Gains/Losses |

| Full amount is taxable | Only half of the amount is taxable (Capital gain/loss x ½ = Taxable capital gain/loss) |

| Business losses are deductible against any form of income made, including business, employment, and property income | Capital losses are deductible only against capital gains |

| If your business loss exceeds your other forms of income, you will only be able to realize the loss up to the value of income for the year E.g., if you have a loss of $500 while your income is $300, you can only use $300 of your loss that year (you will have $200 loss left over) | If your taxable capital losses exceed your taxable capital gains, you will only be able to realize the capital loss up to the value of the capital gains that year E.g., if you have a capital loss of $500 (taxable capital loss of $250) and a capital gain of $300 (taxable capital gain of $150), you can only use $150 of your loss that year (you will have $100 loss left over) |

Once you have determined which transactions are business income/losses, you can start to calculate your net income for tax purposes.

Resources

Buckwold, William, et al. Canadian Income Taxation, 2021/2022. McGraw-Hill Education, 2021.

Wolfe, Kathy. 2022 CPA Competency Map Study Notes, 20th Edition. Densmore Consulting Services Incorporated, 2022.